I was recently asked to talk about how RESP investing in our children’s education funds have changed as the kids get older. If you’re Canadian, you’ll recognize that RESP stands for Registered Education Savings Fund. If you’re reading from another country, the discussion below applies just as much to your own registered or non-registered savings for your children’s college or university education.

This post may contain affiliate links, which means I make a small commission if you decide to purchase something through that link. This has no cost to you, and in some cases may give you a discount off the regular price. If you do make a purchase, thank you for supporting my blog! I only recommend products and services that I truly believe in, and all opinions expressed are my own. As an Amazon Associate I earn from qualifying purchases. Please read my disclaimers for more information.

NOTE: The following article should be considered educational, not direct investment advice. Please consider your own situation before making any savings or investment decisions. See my Terms and Conditions for more information.

What is an RESP?

The Registered Education Savings Plan (RESP) is a government program designed to help families save for children’s post-secondary education costs.

The RESP program has two great benefits:

- When you contribute funds to an RESP, the Canadian government will grant you 20% of your contribution. If you transfer $1,000 to your child’s RESP, you get a $200 grant for free! There is typically a maximum grant of $500 per year up to a lifetime maximum of $7,200 per child, but some families are eligible for more.

- Investments grow tax-free while in the RESP. Withdrawals of grants and income from the RESP are taxed at the student’s marginal income tax rate, which is usually much lower than the parents’ marginal tax rates.

There are limits and rules about RESPs that you can read on the Government of Canada’s website.

Investing versus Savings

You can do any combination of savings and investing in your education fund. This can – and should – change as your children get older.

RESP Savings

Savings do not have any risk of losing money. You deposit funds, and in the future you have at least that amount to take out again. Savings typically have very low rates of return, because they are zero risk. You can save in a regular bank account, a high-interest savings account, or a GIC (guaranteed investment certificate).

RESP Investing

Investing does carry a risk of losing money. You buy an investment product, and hope that it increases in value. But sometimes it does not, and in the end you have less money than you started with. To compensate investors for taking that risk, on average investments have higher returns than savings.

Examples of financial investments are bond funds, stocks, mutual funds (groups of stocks or bonds that are highly managed), and exchange-traded funds or ETFs (groups of stocks or bonds that are NOT highly managed).

Share with someone who needs to read this! 📌

Full-Service versus Self-Directed RESP Investing

When we set up our first education fund, it was the year 2000 and our first child was a newborn. Mr. Tea and I were comfortable investors, and our investments were through Bank of Montreal, with the advice of an investment planner.

We chose this route for several reasons:

- This was a bank and investing format that we were familiar and comfortable with.

- Using mutual funds, we could contribute monthly and reinvest any dividends automatically, with no trading fees.

- When the CESG grants came into the accounts, they were automatically invested and in the same proportion to our overall account objectives.

- Self-directed investing options, and in particular low-cost ETFs, were not nearly as prominent in 2000 when we first started out.

If I were setting up an RESP investing account now, I would likely choose no-fee ETF investing with Questrade. You can contribute each month or whatever schedule suits you best. And you can reinvest any dividends as often as you like. All without any trading fees when you invest in ETFs. It requires a bit more hands-on effort, to remember to invest those funds rather than letting them sit as cash, but the process is simple. With Questrade you can also buy savings products such as GICs. Questwealth offers low-fee portfolios designed by their in-house experts to suit your needs, if you want a little more help.

What do we have in our Education Funds?

We chose mutual funds that tracked the stock market index, and had – for mutual funds – low management expense ratios. Our education fund portfolios includes the following mutual funds:

- BMO Canadian equity ETF fund

- BMO U.S. equity ETF fund

- BMO international equity ETF fund

- BMO bond fund

Canada is a small-ish country in terms of its stock market, and it’s important to diversify across countries, which we do with the U.S. and international equity funds.

The Role of Stocks, Bonds, and GICs

We chose to invest in a general bond fund as a hedge against stock market volatility and have a more balanced portfolio. Returns with bonds tend to be less than in stocks. You miss out on some of the highs, but don’t suffer as deep lows in market downturns. This is a personal preference, and you could choose to be as high as 100% stocks in the early years.

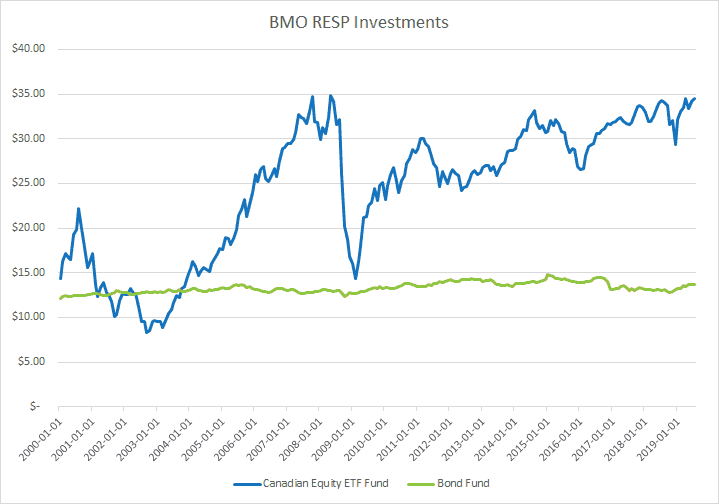

This graph shows the ups and downs of a Canadian equity ETF fund versus a Canadian bond fund. The bond fund is fairly steady over many years, consistently paying out income which is reinvested every month. In contrast, the equity fund experienced incredible gains but also huge losses. Investing in a mix of equity and bonds can act as a buffer during the bad times.

GICs, or guaranteed investment certificates, are a savings option, not an investment. The difference is that your money in a GIC is guaranteed. When you purchase a GIC, you know upfront the interest rate you will receive. There are no ups and downs, like the stock market.

As you get closer to needing those education savings, it’s important to lock in the gains you’ve made over the years. Imagine a stock market crash of 20% the year before your child graduates high school! If your retirement fund took a hit like that, you could probably choose to work a couple of extra years while the market recovered. But you can’t tell an 18-year-old to stay in high school for a few more years!

Hear my interview on RESPs with Explore FI Canada!

We had so much to say about RESPs, Explore FI Canada produced two episodes. The first focuses on basics, including grants, contributions and investments. The second discusses RESP withdrawals, payments and taxation!

- All About RESPs (Part 1) | Money in Your Tea and Modern FImily

- All About RESPs (Part 2) | Money in Your Tea and Modern FImily

Investing and Saving in our Children’s Education Funds

By the end of 2020, my children will be ages 20 (Amber* is in third year of university), 18 (Chris* is entering university), 15 (Phillip* is in high school) and 11 (Audrey* is in elementary school).

Why is this important?

While it is possible to set up a single “family” RESP for all your children, we have opted to set up a separate RESP for each child. I find this more straightforward when making investing and savings decisions, as they are at such different stages!

With Amber in university, all of her RESP is in secured savings products, mainly GICs. This is not the time to take excess risk and hope for wild gains, but potentially lose in a down market. We have already withdrawn a portion of her RESP to pay for her university expenses to date.

Chris is nearing the time when he, too, will need to access the RESP funds to pay for university. We have recently reallocated his account to be fully in savings products, mainly GICs.

Phillip is still three years away from post-secondary. We are slowly starting to move some of his RESP investing away from ETF equity index funds and into GICs. Each year we will continue to move towards locking in his earnings.

Audrey’s RESP investing is mainly in equity ETFs, a mix of Canadian, U.S., and international funds.

Should you Invest Once Each Year or a Bit Every Month?

If you have the full RESP contribution, research shows you are more likely to generate higher wealth by investing it all now. Trying to time the market by contributing a little each month is generally not as profitable.

If you don’t have it all saved up, it’s better to contribute what you can each month, rather than wait.

The old adage hold here: it’s time in the market, not timing the market. Make your contributions, whatever size they are, as soon as you can.

Read my full analysis of why this is true at How to Invest a Lump Sum.

The Takeaway

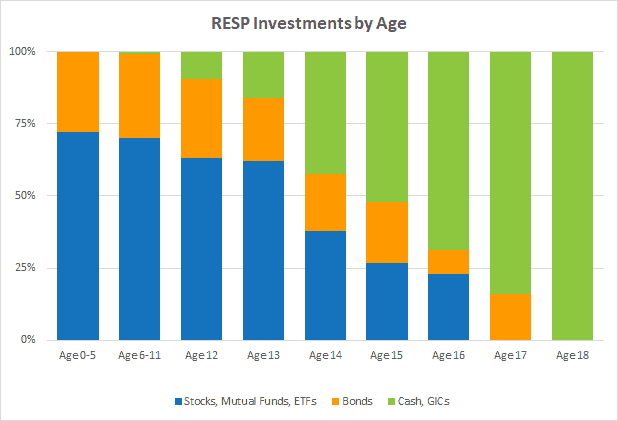

When investing for your child’s education fund, their age is the most important factor in deciding how to invest. Post-secondary typically starts the year they turn 18.

- If your child is grade 6 and under, you have many years left for the stock market to rebound if it crashes. Feel free to invest in as much equity as you are comfortable with. Bond funds are a good choice to pair with equity funds as a buffer.

- If your child is in grade 7-8, start moving to GICs or other secure forms of savings. At this point, if the market took a dive, you still have time to make back some losses. But you want to lock in some of the gains you’ve earned so far.

- If your child is in high school, you have little to no time left to make back losses from a stock market downturn. Plan on being 100% in GICs or other secure savings by grade 11.

Related Reading:

- How to withdraw funds from your RESP

- How to use savings in an RESP

- Bonds, stocks, mutual funds and ETFs

* I use pseudonyms for our children because I feel they should define their own online presence.

Pingback: RESPs in Canada - All Your Questions Answered - Handful of Thoughts