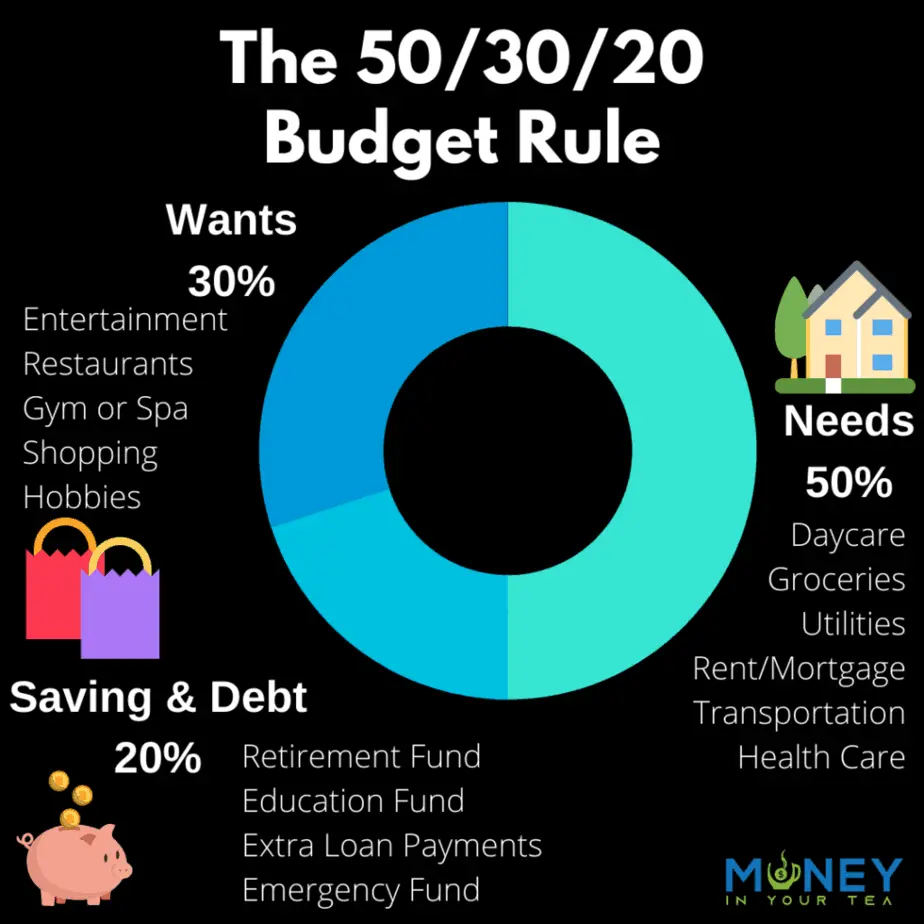

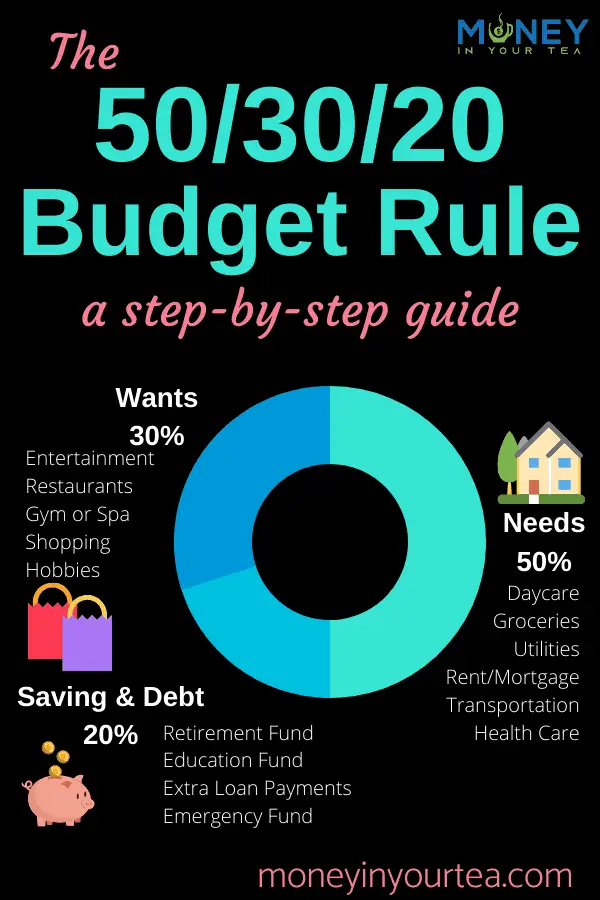

The 50/30/20 budget rule is a simple and intuitive plan to help you reach your financial goals. You allocate 50% of your after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. Budgeting doesn’t have to be intimidating. And it doesn’t have to mean giving up your latte. But in order to be financially responsible and we do need to have a certain level of tracking. And in order to retire someday, in relative comfort, we need to be saving some of our income for the future.

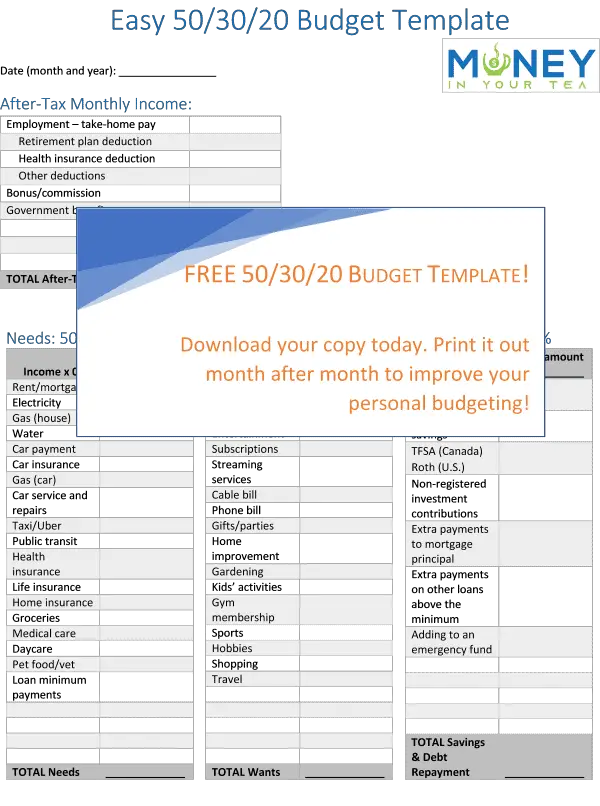

I’ve designed a FREE custom 50/30/20 budget template, just for you! It has many of the standard spending items already filled in for you, so you can spend less time on your budgeting. Simply save the PDF file, and print it off each month! Can’t wait? Skip right to the end to download your free 50/30/20 budget template now.

This post may contain affiliate links, which means I make a small commission if you decide to purchase something through that link. This has no cost to you, and in some cases may give you a discount off the regular price. If you do make a purchase, thank you for supporting my blog! I only recommend products and services that I truly believe in, and all opinions expressed are my own. As an Amazon Associate I earn from qualifying purchases. Please read my disclaimers for more information.

Where did the 50/30/20 Budget Rule Come From?

The 50/30/20 budget rule was popularized in the book “All Your Worth: The Ultimate Lifetime Money Plan“, authored by U.S. Senator Elizabeth Warren, and her daughter, financial consultant Amelia Warren Tyagi.

If you can’t figure out why you work hard, make a decent income, but still feel like you’re living paycheque-to-paycheque then this budget plan is for you.

With great reviews like the one from James below, you may want to pick up a copy for yourself.

I’ve read it too, and found it to be clearly written and non-judgmental. Even though it’s written by American authors, it applies just as much to people in Canada like me, or to the reviewer James, from the U.K.

What are the Three Categories included in the 50/30/20 Budget Rule?

The 50/30/20 budget rule divides your after-tax income into 3 categories: 50% for needs, 30% for wants, and 20% for saving or debt repayment.

Sometimes it’s hard to tell when a particular spending item is a “need” or a “want”. Just give it your best guess. There’s no one judging whether you get this right.

But the first step is to find out what is your typical monthly take-home income.

Step 1: What is your After-Tax Income

The first step in the 50/30/20 budget rule is determining how much income you have coming in each month. Couples should, in most cases, combine their income and spending numbers for the purposes of budgeting, even if you keep separate bank accounts.

Employment Income

If you are a salaried employee, this step is fairly easy. Just look at your pay stubs, and the amount deposited is your after-tax income. This is also known as your take-home pay.

Does the 50/30/20 rule include 401(k) or employer pension contributions? Yes it does.

Look a little closer at that pay stub. If your employer contributes to a retirement plan on your behalf, add that money back in since it’s really part of your paycheque. Employer deducted contributions to your retirement plan are part of your savings, so keep that number handy for Step 4.

Similarly, if your employer deducts funds for health insurance premiums, union dues, or other items, add those back in to get your true after-tax income.

Other Income

If you work on a contract basis, work seasonally, or work for yourself, this step may be a bit more complicated. The easiest method might be to look at your income tax return from last year, see what your net income was, and subtract your income taxes.

Remember to add in other sources of income, such as government transfer payments for child benefits, tax refunds, and so on.

If you have any rental income, remember to subtract costs associated with that to find your net income.

For anyone with unpredictable income such as commission, annual bonus, or seasonal work, the best approach is to calculate your yearly income and divide by 12 to get your average monthly income.

The 50/30/20 Budget Rule

Now that you have found your average monthly income, after taxes, it’s a simple calculation to find out how to allocate that to needs, wants, and saving.

Here’s a 50/30/20 budget example, for four different monthly after-tax income levels.

| Monthly After-Tax Income | $1,500 | $4,000 | $6,000 | $10,000 | ||||

| 50% Needs | $750 | $2,000 | $3,000 | $5,000 | ||||

| 30% Wants | $450 | $1,200 | $1,800 | $3,000 | ||||

| 20% Saving & Debt Repayment | $300 | $800 | $1,200 | $2,000 |

If you earn $4,000 per month in after tax income, then you can spend up to $2,000 on your needs, $1,200 on your wants, and then put the last $800 towards paying down debt or saving for the future.

Step 2: Needs are 50% of Income

Half of your after-tax income should be allocated to paying for your “needs”. These are the things that would be life-changing if you had to do without them. This should be considered a maximum; that is, no more than 50% of your income should go to needs. It includes the following:

- Rent or mortgage (but not the “extra payments” to pay the mortgage faster)

- Utilities such as electricity and gas and water

- Transportation costs, including car payments, insurance, gas, servicing and repairs, as well as taxi/Uber, public transit, or cycling if you use any of these methods to get around

- The minimum payments on any loans, lines of credit, or credit card debt

- All types of insurance, including health, life, disability, home etc.

- Groceries, but not any other food or drink

- Medical care such as health costs, dental, prescription glasses and vision tests, medications, and any other items such as physiotherapy

- Daycare for your child so that you can work

- Basic pet care costs such as food and vet

- Grooming essentials, such as regular haircuts or other things that keep you employable and nice to be around

Notice that some of the things in this list will be fixed expenses that aren’t easily changed, such as your mortgage payment. But others may have a bit of flexibility, such as the types of groceries you buy or shopping at a discount store. Check out some great ideas to save thousands of dollars each year on your food bill.

Step 3: Wants are 30% of Income

Wants are the fun things in life, the experiences and purchases that bring joy and memories. But we’re not cutting all the fun out of life! We’re still spending 30% of our after-tax income on things such as:

- Entertainment – tickets to the big game, going to the movies, memberships, subscriptions, and so on. Netflix and cable TV both fall in this category, as they’re not “needs”

- All non-grocery food and drinks, including alcohol and bars, restaurants and take-out, the daily coffee shop latte (though making it at home falls under “need”)

- Charity – I would classify this as a “want” but if it feels like a “need” to you then feel free to put it in that category

- Gifts and parties

- Home improvement, furnishings, and other home and garden expenses

- Kids’ activities, sports, camps, and so on

- Gym membership, hobbies, teams and social expenses for yourself

- Manicures, spa days, etc.

- Extra pet costs, such as toys, grooming, doggy daycare

- Shopping for clothes (except as required for work), books, electronics, hobbies, sporting goods, and more

- Travel

Note that 30% is considered the maximum you should be spending on wants.

If your spending in this category is higher than 30%, consider where you can cut back. After all, these are all “wants” and so in theory anything should be on the table. See how my family saves $800 per year on cable, internet and home phone.

Step 4: Saving and Debt Repayment are 20% of Income

Your future you will thank the current you for this! Put at least 20% of your after-tax income towards savings and debt repayment. These contributions increase your net worth, which is amazing. Savings and debt repayment includes:

- Retirement savings, including any employer contributions from your pay stub

- Saving in an education fund for your children’s future – help them avoid crippling student loan debt

- Other savings, such as TFSA in Canada, Roth accounts in the U.S., or non-registered investment savings

- Paying more than the minimum payments on your credit card debt, lines of credit, or other loans

- Extra payments on your mortgage that go straight to the principal, helping to pay off that mortgage faster

- Building an emergency fund (start with $1,000, and work up to 3-6 months of expenses)

Unlike wants and needs, this 20% toward savings and debt repayment is considered a minimum amount. If you spend less in the first two categories, feel free to save more than 20%.

Also, if you are planning to retire extremely early, you will need to boost your savings rate to much higher than 20%.

How did you do?

If you live in a high cost-of-living city, you may need to allocate more than 50% of your budget to your needs simply because the housing is so expensive. If you adjust that to 55%, then wants should fall to 25%. Don’t touch the 20% savings category.

If even this is not realistic for you, then you might want to take a hard look at your situation. Moving to a cheaper apartment or house can free up $1,000s each year. Especially if you move away from your high cost-of-living city to somewhere else.

The other approach is to increase your income. Can you rent out a room in your home, get a promotion or raise at work, find a new job that pays more, take on a part-time job, or anything else that will bring in extra money each month.

Related Reading to Bring in More Income:

Who Doesn’t the 50/30/20 Budget Rule Work For?

Is the 50/30/20 budget rule good? While millions of people have found this budget to be just the thing they need to get their spending on track, it doesn’t work for everyone. Here are a few examples.

Higher Income Earners

If you have already paid off your house, first of all congratulations! I’m slightly envious. But that aside, your housing costs have gone down quite a bit right there. You may find that you don’t need anywhere close to 50% of your income for your needs.

If you have lived in your house for a long while, you probably have received many promotions and raises over the years. However, your mortgage payment may still be the same as when you bought the house 15 years ago. Again, you may find that you don’t need 50% of your after-tax income to cover your needs.

Low Income Earners

New graduates may find the opposite problem, where you’re earnings are low and you’re used to living a frugal student lifestyle. You may find much more than 50% going toward needs, while you spend hardly anything on wants.

In addition, if you’re saddled with high student debt, you don’t want to suddenly increase spending on “wants” simply because the 50/30/20 budget rule says you can. In that case, you may want to put much more than 20% toward debt repayment, and live on a shoestring budget. If you can live at home, your “needs” might be mostly taken care of while you tackle that debt.

Late Savers

If you find yourself nearing 50 and you haven’t really started saving for retirement, then you will need to prioritize that by drastically increasing your savings rate. 20% will not be enough in order for you to retire and maintain your current lifestyle.

Retirees

If you have already retired, you may be completely out of debt, with a paid-off house, and you are no longer saving for retirement.

In addition, your income has probably fallen somewhat since you retired.

Looking for a different way to budget? Check out the Highlighter Budget (for everyone who hates spreadsheets!)

Why the 50/30/20 Budget Rule Works for Most of Us

The 50/30/20 budget rule works really well to visualize dozens of spending items into only three basic categories. It will help you evaluate your current spending choices, while also giving you the flexibility you desire to prioritize the things that mean the most to you.

It is an intuitive and simple plan to help you reach your financial goals.

FREE 50/30/20 Downloadable and Printable Budget Template!

Need a little motivation to get going? I’ve created a FREE 50/30/20 budget template just for my readers!

This handy budget tracker comes as a printable PDF file downloadable immediately. No waiting for something to arrive in the mail, and losing your motivation. It’s got all the main needs and wants and savings categories filled in for you, plus a few blanks to write in your own! Print off a new copy every month, and see how your budget is changing as you start to accomplish your financial goals!

If you’re not seeing my form to get your free budget template here, try turning off your ad blocker!

Occasional Expenses

Let’s face it, most of us aren’t taking big vacations every month. This lumpy sort of spending can really throw off your monthly budget if you don’t plan for it.

Once you’ve mastered the 50/30/20 budget rule, and you’re spending within your limits, put anything extra toward a “sinking fund” for these occasional expenses. You may even wish to set up a separate bank account strictly for your sinking fund, and track how much is for which category. Don’t spend your whole sinking fund on a fabulous vacation the year before you will need a new car!

Occasional expenses include:

- Buying a new car (or new to you) if you pay for it outright instead of financing

- Major car repairs

- A big renovation or repair on your house

- Vacations

- Annual vet visits (pets are expensive!), or anticipating future vet needs for a senior pet

- Annual membership fees

- Holiday gifts and other expenses

- Summer camp

- Tuition

Wrapping it all up

Few people like details spreadsheet budget tracking. The 50/30/20 budget rule is a perfect approach to keeping your spending and saving in line, without having to micro manage every little thing. If you’re new to setting a budget, try this approach and let me know how it goes!

And remember to pick up your motivational budget tracker to keep you focused on your goals!

what type of budget would you recommend for people who are already retired

Hi Nancy. I’m so glad you asked! I just wrote about retirement budgeting and I hope you find this helpful. Check it out at https://moneyinyourtea.com/retirement-budget/.

Pingback: The 50/30/20 Budget Rule - FINANCIALEARNER

Pingback: Personal finance articles I loved in November 2019 | Our Bill Pickle

Pingback: Debt Avalanche vs. Debt Snowball - Dividend Power